How an Exchange Works

How a Financial Exchange Works¶

A Conceptual Introduction for Software Developers

No code. No fear. Just the concepts you need to understand the system you are building.

Part I: Foundation , Markets, History, and Participants¶

Context, vocabulary, and the people that define exchange markets , the foundation you need before the mechanics make sense.

Historic Notes

In 1609, a Dutch merchant named Isaac Le Maire organised a consortium of traders to sell shares in the Dutch East India Company (VOC) that they did not yet own. The plan was to drive down the price and buy the shares back cheaply before delivery, the first recorded large-scale short selling operation in financial history. The scheme was brazen enough that the Amsterdam city council attempted to ban short selling the following year. The ban failed. Le Maire was undaunted: he had grasped something fundamental about financial markets that would take regulators centuries to fully accept. Markets are not just places where things are bought and sold. They are environments in which participants constantly probe the rules, exploit information asymmetries, and invent instruments to express views that the market has never had to handle before. The job of exchange infrastructure , the order books, the matching engines, the risk controls, and the audit trails, is to provide a fair, stable, and trustworthy arena for all of this to happen, without breaking when the participants are clever, aggressive, or occasionally reckless.

Every section of this Part can be traced, directly or indirectly, back to what was happening in Amsterdam in 1602 when the VOC issued the world's first publicly traded shares. The primary market, the secondary market, the concept of equity, the vocabulary of long and short, the role of brokers, the need for a central marketplace, it was all there, in embryonic form, four centuries ago.

Part I builds that foundation.

Part Summary:

Build the conceptual base: why exchanges exist, how capital formation connects to secondary trading, how market language evolved, and who the key participants are in modern venues.

Learning Objectives:

- Explain the economic purpose of exchanges in the broader capital-raising cycle.

- Distinguish primary vs secondary markets and debt vs equity at a practical level.

- Use core market vocabulary confidently in historical and modern context.

- Identify major participant types and their incentives in real-world exchange ecosystems.

Content:

- Before the Exchange: How Companies Raise Capital

- What Is a Financial Exchange, and Why Does It Exist?

- The Language of the Market: A Short History

- The Participants

- A Brief Tour of Real-World Exchanges

- Listing and Delisting Mechanics

Before the Exchange: How Companies Raised Capital¶

To understand why a financial exchange exists, you first need to understand why anyone bothers issuing shares in the first place. This section is a brief detour into basic corporate finance, the world your exchange is built to serve.

The Problem of Growth¶

Imagine a small software company. It has a product, a team, and paying customers, but it wants to grow: hire more engineers, open offices in new countries, and invest in research that will take three years to generate revenue. All of that costs money, far more money than the company currently earns in a month or a quarter.

Where does that money come from? There are three broad categories of answer, and real companies use all three at different stages of their lives.

Option 1: Retained Earnings (Self-Funding)¶

The simplest source of capital is the company's own profits. If the company earns more than it spends, it can save that surplus and invest it in growth. This is called retained earnings, profits "retained" in the business rather than distributed to owners.

Self-funding is attractive because it involves no outside parties and no obligations. The problem is that it is slow. If the opportunity is time-sensitive, a competitor is building the same product, or a market window is closing, waiting years to accumulate enough internal cash may mean losing the race. Most high-growth opportunities require more capital, faster, than retained earnings can provide.

Option 2: Debt, Loans and Bonds¶

The second option is to borrow money. Borrowed money must be repaid, with interest [3]. The cost of borrowing (the interest rate) depends on how creditworthy the borrower is: established, profitable companies with predictable revenues can borrow cheaply; young, risky startups may not be able to borrow at all, or only at very high interest rates.

Bank loans are the most familiar form of debt. A company borrows a sum from a bank and repays it over time. This works well for small amounts and short timeframes, but a single bank may not be willing, or able, to provide hundreds of millions of dollars to a single borrower.

Bonds solve the scale problem by spreading the borrowing across many lenders. A bond is a standardised piece of debt. A company issues a bond with a face value (say, $1,000), a coupon rate (say, 5% per year), and a maturity date (say, 10 years from now). The investor who buys the bond lends the company $1,000 today. In return, the company promises to pay $50 per year (5% of $1,000) as regular interest payments (these periodic payments are called coupons, named after the physical coupon slips investors used to cut off and redeem before the digital age), and to repay the full $1,000 when the bond matures in 10 years.

A large company might issue millions of these bonds simultaneously, raising hundreds of millions of dollars from thousands of individual investors. Those investors later need to be able to sell their bonds if they want their money back before maturity, and so bonds, just like shares, trade on exchanges and electronic markets.

The key characteristic of debt: the company has an unconditional obligation to make the promised payments. If it cannot, it is in default, which can lead to bankruptcy proceedings. Bondholders are creditors: they have a legal claim against the company's assets. In a bankruptcy, creditors get paid before the company's owners.

Option 3: Equity, Selling Ownership¶

The third option is fundamentally different in character: instead of borrowing money and promising to repay it, the company sells a piece of itself.

Equity is ownership. When a company issues shares (also called stock in American English, or equities in market terminology), it is dividing ownership of the business into small, standardised units and selling those units to investors [3]. Each unit, each share, represents a proportional claim on the company's assets, earnings, and future.

Here is the important distinction from debt: there is no promise of repayment. If you buy a share in a company, the company does not promise to give your money back. It does not promise to pay you any specific amount at any specific time. What you receive instead is ownership.

What does ownership actually mean?

-

Residual claim on profits: If the company earns a profit and its board of directors decides to distribute some of that profit to owners, shareholders receive their proportional share as a dividend. Dividends are not guaranteed, the board may decide to reinvest profits in the business instead. But shareholders are entitled to whatever is left over after all expenses and debts are paid. This "residual" or "leftover" claim is the defining characteristic of equity.

-

Capital appreciation: If the company grows and becomes more valuable, each share becomes worth more. A shareholder who paid $10 for a share and sells it when the company is worth twice as much can sell at roughly $20, realising a capital gain. The theoretical upside of an equity position is unlimited, a share can appreciate many times over (Apple has multiplied in value hundreds of times since its IPO). Compare this to a bond, where the return is capped at the promised coupon rate.

-

Voting rights: Shares typically carry the right to vote on major corporate decisions, electing the board of directors, approving mergers and acquisitions, and other significant matters. Owning 51% of the shares means controlling a majority of votes, which is why "controlling stake" is a meaningful concept.

-

Limited liability: If the company goes bankrupt, shareholders can lose the money they invested, but nothing more. They are not personally liable for the company's debts. This protection ("limited liability") is a fundamental feature of the modern corporation and one reason equity investment became widespread.

-

Market capitalisation (market cap): The total market value of all a company's outstanding shares, calculated as share price multiplied by the total number of shares in existence. If Apple has approximately 15.4 billion shares outstanding and each trades at $190, Apple's market cap is roughly $2.9 trillion [1]. Market cap is the most widely used shorthand for a company's size. When rankings refer to "the world's largest exchange by listed market cap," they are summing the market caps of every company listed there.

What does ownership mean for the company?

Issuing equity capital has an important advantage over debt: the company is not obligated to make regular payments, and there is no maturity date on which it must repay anything. This flexibility is why many high-growth companies prefer equity, they can invest in long-term projects without the burden of fixed interest payments.

The trade-off is dilution: selling shares means selling a portion of the company. The founders and early investors own a smaller fraction of the whole. If a founder owned 100% of a company worth $1 million and raises $250,000 by selling a 20% stake to new investors, the company is now worth \(1.25 million (\)1 million of existing business value plus the $250,000 cash just raised). The founder owns 80% of $1.25 million, still $1 million in absolute terms, but a smaller fraction of the whole. The investors own 20% of $1.25 million = $250,000, exactly what they paid. Managed carefully, dilution is acceptable; managed carelessly, founders can lose control of their own companies.

Common stock and preferred stock

In practice, not all shares are equal. Most retail investors hold common stock (called ordinary shares in UK and European markets), which carries voting rights and a residual claim on profits. Preferred stock (or preference shares) is a different class: typically no voting rights, but a higher-priority claim on dividends and assets in a liquidation. Preferred holders are paid before common stockholders, though still after bondholders. Venture capital investors almost always receive preferred stock in early-stage companies, giving them downside protection that common stockholders lack [3].

When a company IPOs, most preferred shares convert to common shares. For exchange system developers, the class distinction matters because instruments are classified, regulated, and referenced differently. When you see "AAPL" on an exchange, it refers specifically to Apple's common stock. Preferred shares, if listed, trade under a different ticker (typically something like "AAPL-PRA").

The Difference Between Debt and Equity¶

A useful mental model: when a company issues bonds, it is renting capital, borrowing it with the obligation to return it. When a company issues equity, it is selling a permanent stake, the investor becomes a partial owner, sharing in the future of the business.

The consequence:

| Debt (Bonds, Loans) | Equity (Shares) | |

|---|---|---|

| Relationship to company | Lender / Creditor | Owner |

| Return | Fixed interest (coupon) | Variable (dividends + capital gains) |

| Repayment obligation | Yes, principal returned at maturity | No |

| Payment priority in bankruptcy | Paid first | Paid last (residual) |

| Risk to investor | Lower (predictable return) | Higher (no guaranteed return) |

| Dilutes ownership? | No | Yes |

| Upside potential | Capped (only the promised coupons) | Unlimited (shares in a successful company grow without limit) |

A sophisticated investor builds a portfolio that mixes both: bonds for predictable income and capital preservation, equities for growth potential. The entire investment industry, pension funds, mutual funds, hedge funds, is built around managing this balance.

Going Public: The Initial Public Offering (IPO)¶

Early in a company's life, its shares are held by a small, private group: the founders, early employees (who often receive shares as part of their compensation), and venture capital (VC) investors who provided early funding in exchange for equity stakes. These shares are not available to the general public; the company is private.

At some point, usually when the company has proven its business model and needs a large infusion of capital for the next phase of growth, the company may choose to go public: to offer its shares for sale to anyone who wants to buy them. This event is called the Initial Public Offering (IPO).

In an IPO:

- The company works with investment banks to underwrite the offering. Underwriting means the banks agree to buy all the shares at a guaranteed price and immediately sell them on. This guarantee means the company receives its cash even if investor demand is weaker than expected. In practice, the banks first conduct a roadshow, a series of presentations to large institutional investors, to gauge demand and set the final price. They rarely actually get stuck holding the shares.

- New shares are created and sold, with the proceeds going directly to the company (or to early investors who are "cashing out" their stakes).

- The company's shares are listed on a stock exchange, NYSE, NASDAQ, LSE, or another regulated market.

- From that moment, anyone can buy or sell the shares through the exchange.

Some of the largest IPOs in history by proceeds raised illustrate the scale: Saudi Aramco raised $25.6 billion in its 2019 IPO on the Saudi Exchange (Tadawul) [1]; Alibaba raised $21.8 billion on NYSE in 2014 [1]; Arm Holdings raised $4.9 billion on NASDAQ in September 2023 [1]. Each of these companies brought enormous new pools of capital onto public markets.

In recent times, SpaceX's June 2026 IPO on NASDAQ (ticker: SPCX) is the largest IPO by proceeds raised in history. Priced at $135 per share, the offering implied a valuation of approximately $1.77 trillion; shares opened around $150 and closed the first trading day up roughly 19%, putting the company's market cap in the $2.1–2.2 trillion range by the close. Note that pricing a mega-IPO below $200 a share says nothing about the company's quality or size, it is purely a function of how many shares are outstanding relative to the total valuation, which the company and its underwriters can set almost arbitrarily by choosing the share count. (The historical "blue chip" usage described later in this document, where Oliver Gingold's 1923 Dow Jones column used $200 as a rough marker of a premium stock, was itself a nominal dollar figure of its era with no inflation adjustment; it was never a rule, and it says nothing about a company listing a century later.)

The Primary Market vs. the Secondary Market¶

This distinction is critical, and it is where the exchange fits in.

The primary market [3] is where new securities are created and sold for the first time. In an IPO, the company sells newly issued shares directly to investors, and the company receives the money. A bond issuance is also a primary market transaction, new bonds are created and the company receives the loan proceeds.

The secondary market [3] is where investors buy and sell securities that already exist, trading with each other rather than with the company. When you buy shares of Apple on NASDAQ today, Apple does not receive your money. The person selling you those shares receives it. Apple issued those shares long ago; they have been trading between investors ever since.

The stock exchange is among the primary venues of the secondary market. It is the most visible and regulated secondary market venue, but not the only one, OTC secondary trading, private transactions, and alternative trading systems also exist. For practical purposes in this document, when we say "the exchange," we mean a regulated, centralised lit venue; this is where the concepts of price-time priority, order books, and matching engines apply most directly.

This insight is important: the exchange does not help companies raise money directly. It helps investors trade securities they already own. But without the secondary market, the primary market would barely function. Here is why:

Who would invest in a company's IPO if they knew they could never sell their shares? Who would buy a 10-year bond if they had to hold it for exactly 10 years with no way out? The existence of a liquid secondary market, a place where you can sell whenever you want at a fair price, is what makes investors willing to commit capital to companies in the first place. The exchange provides the exit. And the availability of an exit enables entry.

The primary market and secondary market form a virtuous cycle:

- Companies raise money in the primary market because investors are willing to commit capital.

- Investors commit capital because the secondary market lets them exit when they choose.

- The secondary market functions well because many investors participate.

- Many investors participate because companies with real value list their shares there.

The stock exchange, the subject of this entire document, is the infrastructure that makes this cycle turn.

flowchart TD

CO["🏢 Company"]

PM["Primary Market\nIPO / follow-on offering\nCompany receives cash"]

EX["Stock Exchange\nSecondary Market"]

INV["Investors\nBuyers and Sellers"]

CO -- "Issues new shares" --> PM

PM -- "Shares delivered to first investors" --> INV

INV -- "Buy and sell shares\namong themselves" --> EX

EX -- "Price discovery\nand liquidity" --> INV

EX -. "No cash flows back\nto the company" .-> COA Word on Other Instruments¶

The same framework applies to other instruments:

-

Bonds trade on bond markets (some exchange-based, others over the counter) after issuance. Investors can sell their bonds before maturity, receiving the current market price rather than waiting for repayment.

-

Futures and options are not claims on existing assets at all, they are contracts about future transactions [12] [13]. Their markets have their own logic, but the exchange's role (centralised matching, price discovery, fairness) is the same.

-

Exchange-Traded Funds (ETFs) are baskets of shares (or bonds, or commodities) that themselves trade as a single share. iShares, Vanguard, and SPDR products are examples. ETFs trade on exchanges exactly like individual stocks.

-

Market indices are calculated measures of the aggregate performance of a defined basket of securities. The S&P 500 tracks 500 large US companies and is the most closely followed equity index in the world, first published in its current form by Standard & Poor's in 1957. The Dow Jones Industrial Average (DJIA), dating to 1896, tracks 30 large US companies. The NASDAQ Composite tracks all stocks listed on NASDAQ. Indices themselves are not directly tradeable, but index futures (on CME), index options (on Cboe), and index ETFs allow investors to trade the performance of a whole index with a single instrument. When a portfolio manager says "the market is up 0.8% today," they almost always mean the S&P 500. When exchange system developers build risk calculations or position monitors, index levels are frequently the benchmark against which positions are marked.

With this foundation in place, understanding what a share is, why companies issue them, and what role the exchange plays, we can now look at the mechanics of how an exchange actually operates.

What Is a Financial Exchange, and Why Does It Exist?¶

The Core Problem¶

Imagine you own 1,000 shares of a technology company (you understand now what that means: you own a tiny fraction of that company, acquired when you bought the shares from a previous owner on the secondary market) and you want to sell them. Somewhere out there, someone wants to buy exactly 1,000 shares of that same company at roughly the price you have in mind. The problem is finding each other.

Before modern exchanges existed, this "finding" problem was enormous. Stock trading happened in coffee houses, in the street ("Exchange Alley Coffeehouses"), or through networks of personal contacts. One of the first places on record was "Jonathan's Coffee House" (The Forerunner to the London Stock Exchange) founded around 1680 by Jonathan Miles, Jonathan's became the primary gathering place for stock brokers [10]. Prices were inconsistent, you might sell at one price while, moments later, someone else sold the same shares at a very different price. There was no guarantee you were getting a fair deal, and there was no way to know what "fair" even meant.

Auctions by the Candle

Garraway's Coffee House was opened by Thomas Garway and famed for being the first place in England to retail tea (in 1657). It was quickly rebuilt on a grand scale after the 1666 Great Fire. While Jonathan's focused heavily on shares, Garraway's specialised in commodities, hosting the Hudson's Bay Company's first fur auction in 1671 and later auctioning Australian wool.

Garraway's was legendary for its unique bidding system: an auctioneer would light an inch of tallow candle, and the last bid placed before the flame flickered out won the goods. Candle Auction

The golden era of the informal Exchange Alley coffeehouses came to a catastrophic halt on March 25, 1748, when a massive fire broke out in Cornhill, destroying Jonathan's, Garraway's, and nearly 100 surrounding buildings. Though both shops were eventually rebuilt, the financial markets were rapidly moving toward formal, dedicated corporate buildings, leaving the casual coffeehouse model behind.

A financial exchange solves this problem by acting as a centralised marketplace, a single place where all buyers and sellers come together, where prices are visible to everyone, and where agreed rules govern who trades with whom at what price. The NYSE was founded in 1792 under a buttonwood tree on Wall Street [10]; NASDAQ launched in 1971 as the world's first electronic stock market [10]. Both exist to solve the same fundamental problem: matching buyers with sellers fairly and efficiently.

It is worth noting that exchanges are among the most visible matching venues, but not the only ones. Over-the-counter (OTC) markets (where participants negotiate directly), Alternative Trading Systems (ATSs), Electronic Communication Networks (ECNs), and internalisers (brokers who match client orders internally against their own inventory) all also match trades. The concepts in this document apply most directly to regulated exchanges, but the same vocabulary, order book, spread, price-time priority, is used across all these venues.

The Three Promises of an Exchange¶

Every exchange makes three implicit promises to its participants:

1. Price discovery. At any moment, the current price of an asset reflects the aggregate opinion of all participants currently willing to trade it. You can look at the market and see what "fair value" is right now.

2. Liquidity. You can convert your asset into cash (or vice versa) quickly, without having to wait indefinitely for a counterparty to appear. The exchange provides the infrastructure that makes counterparties findable.

3. Fairness and transparency. The rules for who trades first and at what price are known in advance, applied consistently, and visible to all participants equally. There is no backroom dealing.

How Exchanges Are Regulated¶

Exchanges do not operate by custom alone. They are licensed and supervised by government regulators whose rules directly shape how exchange systems are designed and built.

In the United States, equity exchanges are overseen by the Securities and Exchange Commission (SEC), established by the Securities Exchange Act of 1934 in the aftermath of the 1929 crash and subsequent Great Depression. The crash and its causes deserve a sentence of context here, because they explain why the SEC's mandate is what it is.

Between 1928 and September 1929, the US stock market had doubled. Investors were buying heavily on margin, borrowing money to buy more stock than they could afford outright. When prices began to fall in October 1929, margin calls forced widespread selling. Selling drove prices lower, which triggered more margin calls, which drove more selling , the same feedback loop that automated portfolio insurance would recreate in 1987. The Dow Jones Industrial Average fell 89% from its 1929 peak to its 1932 trough. Thousands of banks failed. Millions lost their savings. The subsequent investigation found rampant stock manipulation, insider trading, misleading corporate disclosures, and conflicts of interest at every level of the market. The Securities Act of 1933 and the Securities Exchange Act of 1934 were Congress's direct response: transparency requirements, registration of securities, prohibition of fraud, and the creation of the SEC to enforce the rules. The exchange system you are building operates under the regulatory framework those 1930s laws set in motion.

Several regulations appear throughout this document and in most exchange codebases. It is worth naming them here:

-

Regulation NMS (National Market System, adopted 2005, phased in through 2007): Requires that equity orders receive the nationally best available price across all registered trading venues. This single rule is the reason the US has 16+ registered equity exchanges competing for order flow, and the reason smart order routing exists , brokers must route to wherever the best price is, not just the closest or the cheapest.

-

Regulation SHO (2005): Governs short sales, including the locate requirement (broker-dealers must verify shares can be borrowed before accepting a short sale order) and delivery obligations.

-

Market Access Rule (Rule 15c3-5, 2010): Requires broker-dealers providing market access to have pre-trade risk controls: maximum order sizes, credit limits, and kill switches. Enacted directly in response to the 2010 Flash Crash.

In Europe, the equivalent framework is MiFID II (Markets in Financial Instruments Directive II, 2018), which mandates best execution, algorithmic trading controls (including mandatory kill switch testing), trade reporting, and systematic internaliser reporting. Any exchange system intended to operate in EU markets must comply.

Understanding which regulator and which rules apply is not just a legal matter. It is an engineering specification: audit trail formats, kill switch accessibility, pre-trade check requirements, and market data publication rules are all regulatory mandates, not optional features.

Instruments: What Is Being Traded?¶

An exchange does not trade "things" in a physical sense. It trades instruments, standardised financial contracts representing ownership or obligation. The most common are:

-

Equities (stocks): A share represents a small piece of ownership in a company. When you buy one share of Apple (ticker symbol: AAPL), you own a tiny fraction of Apple Inc. NYSE and NASDAQ are primarily equity exchanges.

-

Futures contracts: An agreement to buy or sell something (oil, gold, a stock index) at a specified price on a specified future date. CME Group is one of the world's largest futures exchanges.

-

Options: The right (but not the obligation) to buy or sell an instrument at a specific price before a specific date. Cboe is a major options exchange.

-

Foreign exchange (FX) pairs: The price of one currency expressed in another, such as EUR/USD (how many US dollars one Euro buys). FX trades largely on electronic networks rather than centralised exchanges, though the principles are similar.

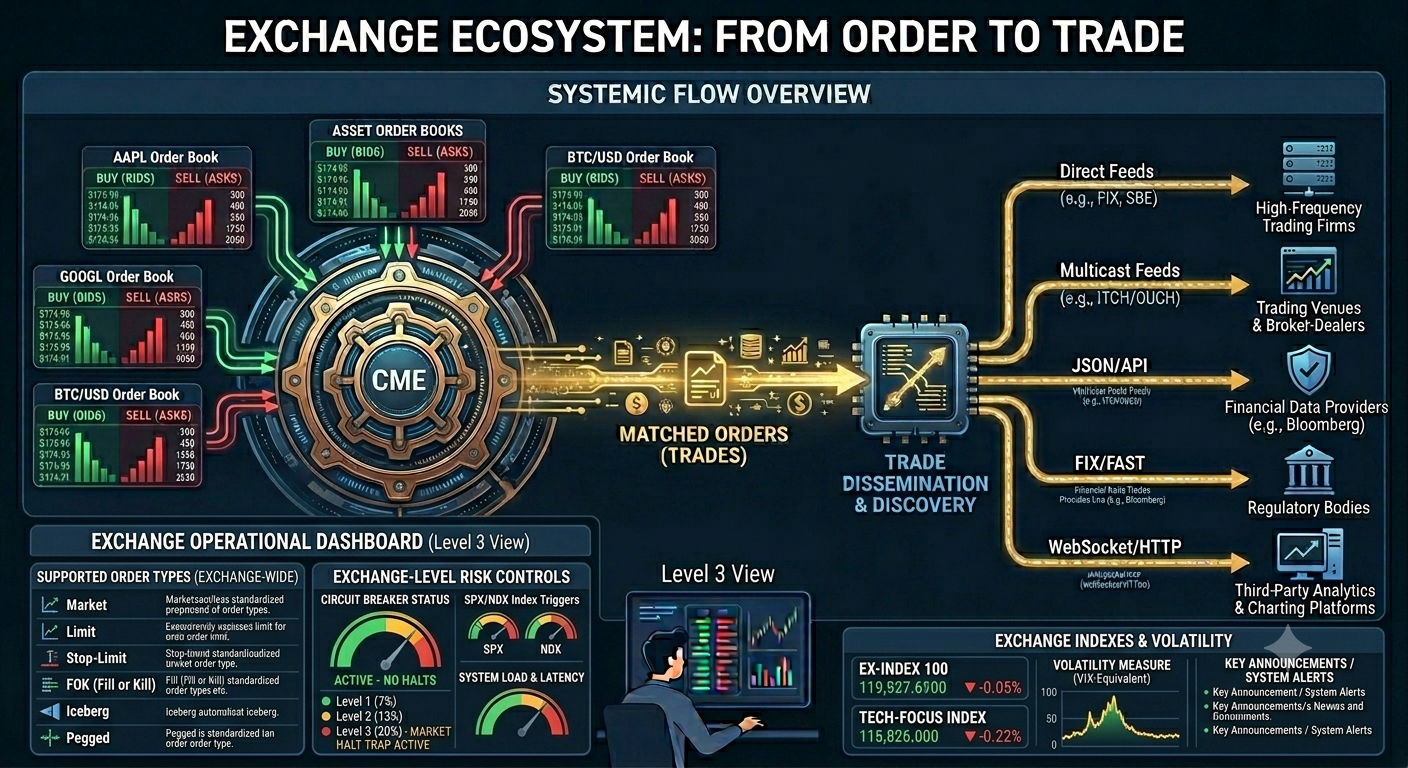

An equity exchange handles each symbol (like AAPL, MSFT, or TSLA) as a separate tradeable instrument, each with its own independent order book.

The Language of the Market: A Short History¶

Before you read about participants, orders, and matching engines, it is worth pausing on something that will serve you well throughout your career working on exchange systems: much of the language you will encounter in this codebase has historical roots that no longer match the physical reality. Terms that sound arbitrary or old-fashioned are fossil words, the language of a world of wooden desks, brass bells, and paper ledgers that gradually evolved into the nanosecond world of today. Understanding where the words came from will make them stick, and will save you from wondering why a system full of cutting-edge software keeps referring to things like "the book," "the tape," and "the floor."

The Physical Book¶

Before electronic trading systems, every major exchange operated a physical trading floor, and on that floor, for every stock, there was a person responsible for maintaining order: in NYSE's terminology, this was called the specialist. The specialist's job was to act as a market maker for their assigned stocks, and to maintain, literally on paper, a record of every outstanding buy and sell order that had been submitted but not yet filled.

This record was kept in a physical ledger book. The book was divided into two columns: one for buy orders (bids) listing each buyer's offered price and quantity, and one for sell orders (asks) listing each seller's demanded price and quantity. The specialist would review the book, try to match buyers with sellers, and maintain an orderly market by quoting prices to floor brokers who came to trade.

When a broker wanted to buy shares and asked "what's the market in IBM?", the specialist would look at their book and say, for example, "fifty-five for five hundred, five hundred at fifty-five and a quarter", meaning the best available buyer was offering $55 for 500 shares, and the best available seller was asking $55.25 for 500 shares. The specialist was reading, live, from their paper book.

The physical book is gone. Every exchange in the world now maintains its order book in computer memory, with data structures designed for nanosecond access. But the name has survived completely intact. When developers and traders today say "the book," "working an order into the book," "resting in the book," or "taking from the book," they are using the exact same language that floor traders used when pointing at a physical ledger. The order book is one of the purest examples of terminology that crossed from physical to digital without losing a syllable.

Open Outcry and the Pit¶

On exchange floors like CME Group's in Chicago, trading in futures contracts was conducted through open outcry, a method where traders stood in a sunken circular area called a pit and literally shouted their bids and asks at each other, using a combination of voice and hand signals to communicate price, quantity, and direction. The noise was enormous. The system worked because the pit was small enough that everyone could hear and see everyone else.

The CME Group operated open outcry pits for decades. Some products, particularly certain agricultural and options contracts, continued in open outcry long after equity markets went fully electronic, largely because the pit handled complex, illiquid products where human negotiation had genuine advantages. CME substantially wound down its open outcry operations in 2015 [9], though some niche trading still occurs. The physical pit is where terms like "floor broker" (a broker who executes trades on the physical floor), "floor trader" (a trader who trades for their own account from the floor), and "pit committee" originated.

The terms survive in documentation, regulations, and informal industry speech even though the pits themselves are mostly silent now.

The Ticker Tape¶

Before electronic screens, prices of completed trades were published via the stock ticker, a telegraph-based machine, invented by Edward Calahan in 1867 [15] and later improved by Thomas Edison, that printed a continuous stream of abbreviated stock symbols and trade prices on a narrow paper tape. The tape moved fast (hence "ticker", the machine made a ticking sound) and the strip of paper would pile up on the floor of brokerages around the country as trades printed in real time.

Reading the tape was a skill. A tape reader was someone who could watch the continuous stream of prices and volumes and infer what institutional buyers and sellers were doing, one of the earliest forms of technical analysis. An even earlier form of market observation appears in Joseph de la Vega's Confusión de Confusiones (1688) [4], the oldest known book about stock trading, written in Amsterdam about the VOC share market, which describes participants reading order flow and inferring intent from patterns of buying and selling.

In 1878, the phone was invented. In 1929, the first electronic ticker was installed. By the 1960s, electronic displays began replacing paper. Today, the "ticker" refers to the digital price feeds streaming across screens in every trading firm, brokerage, and financial news channel, and the ticker symbol (AAPL, MSFT, GOOG) is the abbreviated code printed on the old paper tape.

When you see terms like "tick" (the minimum price movement), "tick data" (a record of every trade), or "ticker plant" (the server infrastructure that publishes market data), you are using the language of a machine that ran on telegraph cables and printed on paper strips.

The Language Lives in the Code¶

These historical terms are not just in trading rooms and textbooks. They are in the source code. A developer reading an exchange codebase for the first time will find:

bid_price,ask_price,spread, the physical ledger's two columns, reduced to struct fieldslot_size,tick_size, the standardisation introduced by the early commodity pitsaggressor_side, which party crossed the spread; matters for fee calculation and regulatory reportingbook.add_order(),book.cancel_order(),book.sweep(), the specialist's actions, now function callsGTC,DAY,IOC, time-in-force codes whose full names (Good-Till-Cancelled, Day, Immediate-or-Cancel) are rarely spoken, used daily in hundreds of millions of orderstape_price,last_trade_price, what the ticker printed, now a field in a trade recordlong_position,short_position, the Amsterdam merchant's grain warehouse, abstracted to a signed integer

Every time you read a function name or a variable name in exchange software that sounds like it belongs in a different century, it does. The codebase is the physical exchange, translated.

Black Monday and the Origin of Circuit Breakers¶

On 19 October 1987, US stock markets fell 22.6% in a single day, the largest single-day percentage drop in the history of the Dow Jones Industrial Average. This event, known as Black Monday, remains the most severe one-day market crash on record. A more detailed account of this is given in the Risk Controls, Protecting the Market section of Part III.

The crash was not driven by a single piece of bad news. It was amplified by automated portfolio insurance programmes, algorithmic selling strategies designed to protect institutional portfolios by automatically selling futures contracts as prices fell. As these programmes sold, prices fell further, triggering more programme selling, which pushed prices further down , a feedback loop that human traders could not interrupt. The lack of any coordinated mechanism to pause trading made the spiral self-reinforcing.

The Presidential Task Force on Market Mechanisms (the "Brady Commission"), reporting to President Reagan in January 1988, concluded that the absence of circuit breakers and coordinated pause mechanisms across markets had allowed the panic to become catastrophic. Its central recommendation was explicit: create automatic trading halts that could interrupt the feedback loop and give participants time to assess [Brady Commission Report, January 1988].

NYSE introduced the first market-wide circuit breakers in 1988 directly in response. The specific thresholds have been adjusted several times since (most recently after March 2020, when Level 1 was triggered four times in two weeks during the COVID-19 crash), but the mechanism traces directly to that January 1988 report.

This history matters for exchange system developers because circuit breakers are not bureaucratic decorations. They are the engineering response to a proven systemic failure mode: automated systems amplifying each other into a catastrophic spiral. Every halt threshold, every resumption auction, every "do not accept orders during HALTED state" condition in a matching engine exists because of what happened on 19 October 1987.

Settling Up: Settlement Periods and Why They Exist¶

The historical reason settlement took multiple days has nothing to do with technology and everything to do with physical logistics. In the era of paper stock certificates, when you sold your shares, you had to physically deliver a paper certificate to the buyer, and they had to physically deliver cash or a cheque to you. Messengers on bicycles carried these documents between brokerage firms on Wall Street. Giving everyone five business days (the original settlement period was T+5) provided time for paperwork to move across Manhattan, be checked, and be processed.

As the industry moved to dematerialisation (electronic records replacing paper certificates) and electronic funds transfer, settlement windows shrank: T+5 became T+3 in the 1990s, T+2 in 2017, and T+1 in 2024 in the US [8]. The "T+N" notation remains standard even as the N shrinks. Some markets are exploring same-day (T+0) settlement, though this requires that cash and securities be available at the exact moment of trading, a more demanding operational requirement.

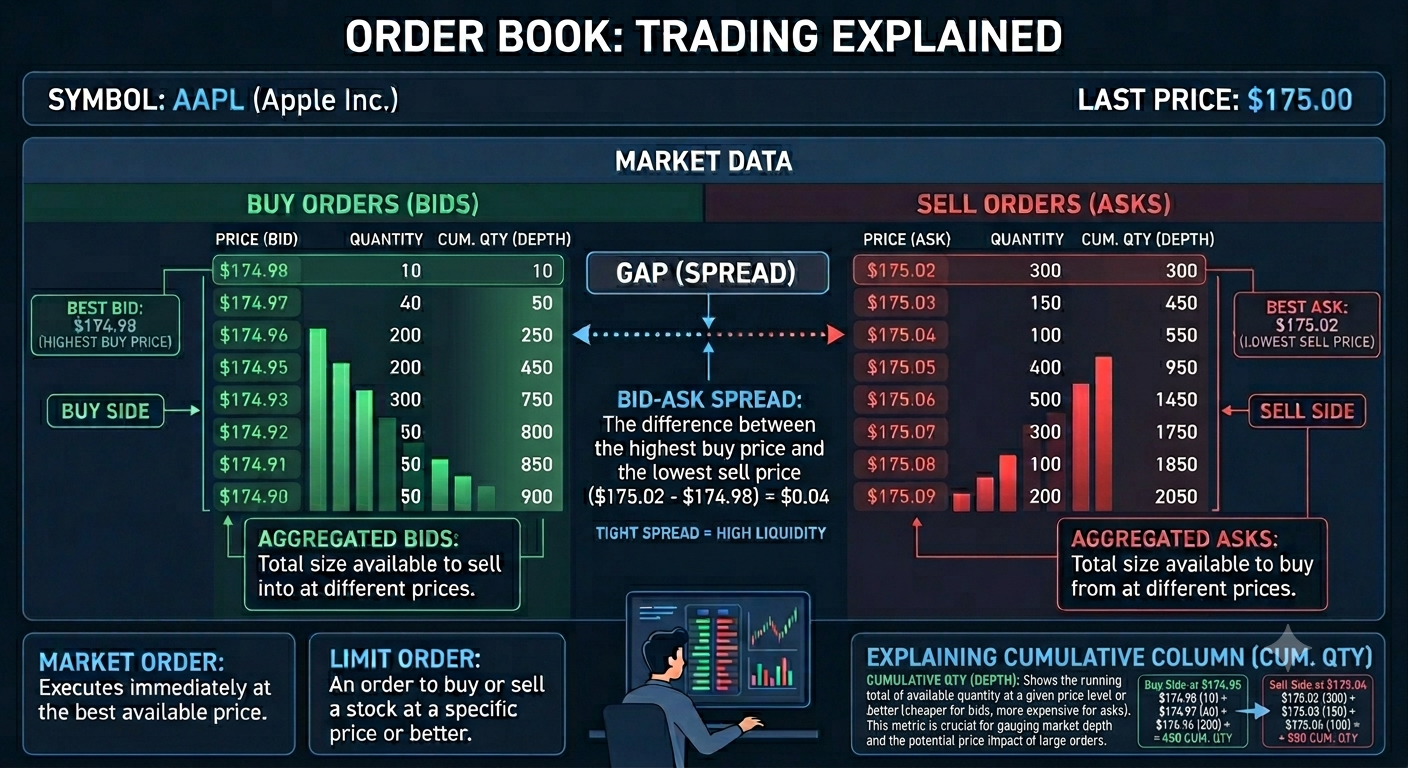

The Bid, the Ask, and the Spread¶

The two most fundamental prices in any market are the bid and the ask (also called the offer in some contexts). These are ancient words in the context of markets.

Bid comes from Old English beodan, meaning to announce, command, or offer. To bid for something is to announce the price you are willing to pay. A bidder at an auction makes a bid; a trader in a market makes a bid. The word has been used in commercial contexts for over a thousand years.

Ask (or offer) is the counterpart: the price at which someone is willing to sell. Asking a price for goods is as old as commerce.

The spread is the difference between the best bid and the best ask at any moment: if the best bid is $150.30 and the best ask is $150.35, the spread is $0.05. The spread is both a measure of market quality (tight spreads mean the market is liquid and efficient; wide spreads mean it is illiquid or uncertain) and the primary source of income for market makers, who earn the spread by continuously standing ready to buy at the bid and sell at the ask.

The phrase "crossing the spread" means submitting an order aggressive enough to immediately match against a resting order. An investor who submits a buy order at $150.35 (the ask) rather than waiting at $150.30 (the bid) is crossing the spread and paying for the privilege of immediate execution. This small payment , a few cents, or a fraction of a cent in liquid markets , is the cost of immediacy, and it is the foundation of the market maker's business model.

Blue Chips, Bulls, and Bears¶

Not all inherited terminology has to do with physical infrastructure. Some comes from adjacent worlds:

Blue chip stocks are large, well-established, financially sound companies, the most prestigious tier of the equity market. The term comes from poker: in casino chips, blue has traditionally been the highest denomination. The first recorded use in finance was by Oliver Gingold at Dow Jones in 1923, who described stocks trading at $200 or more per share as "blue chip stocks." [14]

Bull market (rising prices) and bear market (falling prices) have disputed origins, but the most widely cited explanation refers to how each animal attacks: a bull thrusts its horns upward, a bear swipes its paws downward. The terms appear in financial writing as early as the 18th century. Today, a market that has fallen 20% or more from a recent peak is formally defined as a bear market; a sustained rise of 20% or more from a trough is a bull market.

Going long and going short have roots far older than stock markets. Their origin lies in the physical trade of commodities, grain, spices, metals, cloth, timber, and other durable goods, that dominated commerce for centuries before financial securities existed.

A merchant in a 17th-century Amsterdam or London trading house who had purchased a large stock of grain and was storing it in a warehouse was described as being long in grain [4]. The word captured two ideas simultaneously: first, that they possessed the goods, they owned something tangible, in their hands, in their warehouse; and second, that durable goods could be held over time. Grain kept through winter. Spices kept for years. Metal did not spoil. A merchant who was "long" in such goods had an inventory that would last a long time, goods with longevity. The root connection is direct: long as in duration, as in possession extended through time.

This is still exactly what "going long" means in modern finance: you own the asset and you are exposed to its price over time. If you buy shares of a company and hold them, you are long those shares. If the price rises, your long position profits; if it falls, it loses. Nothing about the meaning has changed, only the asset has shifted from sacks of grain in a warehouse to electronic records in a clearing house.

Going short comes from the opposite situation: a merchant who had promised to deliver goods they did not yet possess. In forward contracts, common in the grain and commodity markets of the 17th and 18th centuries, a seller would commit to deliver a quantity of goods at a future date and price. If they had sold more than their warehouse contained, they were "short" of the goods, deficient, lacking, falling short of their obligations. The same word family as "we are short of supplies," "he fell short of expectations," or "shortage." Being short meant your inventory was insufficient to cover what you had committed to deliver. You would need to go into the market and buy before the delivery date, hoping prices had fallen so you could profit on the difference.

The Dutch East India Company (VOC), founded in 1602 and traded on the Amsterdam Exchange from that same year, pioneered many instruments still in use today, transferable shares, dividend payments, and the secondary market in those shares [5] [11], and became the arena for what is likely the first recorded large-scale short selling operation in financial history: in 1609, a merchant named Isaac Le Maire organised a group of traders to sell VOC shares they did not own, betting the price would fall so they could buy them back cheaply before delivery [5]. The scheme was disruptive enough that the Amsterdam city council attempted to ban short selling the following year, the earliest known attempt to regulate the practice [5]. It did not stick; short selling has been controversial, periodically banned, and always present in markets ever since.

"Long" and "short" thus carry the physical memory of a world where trading meant moving real goods between warehouses and ships. A developer reading last_sell_price or position += signed_qty in the matching engine's clearing code is working with concepts that a 17th-century spice merchant would have recognised immediately, even if the technology would be unrecognisable to them.

The Operational Mechanics of Short Selling, Borrow and Locate¶

The historical explanation above describes the economics of short selling. The modern operational reality involves several additional steps that are invisible in the exchange's order book but fundamental to how clearing and settlement actually work.

You must borrow before you short. Before a participant can sell shares they do not own, they must first arrange to borrow those shares from someone who does own them. This is called the locate process, finding and reserving a source of borrowable shares. In the US, Regulation SHO (adopted by the SEC in 2005) mandates that broker-dealers must have a reasonable grounds to believe shares can be borrowed before accepting a short sale order. Selling short without a locate is called naked short selling and is generally illegal.

Where the borrow comes from. Shares available to borrow come primarily from long investors who hold shares in custody through a broker or prime broker. These holders consent (usually automatically through their account agreements) to their shares being lent out in exchange for a lending fee. The custodian or prime broker intermediates: they find willing lenders and lend the shares to the short seller. The short seller pays a daily lending fee (the borrow rate) while the position is open.

Borrow rates and hard-to-borrow stocks. Most large-cap, liquid stocks are "easy to borrow", borrow rates are near zero because many shares are available. Smaller, heavily-shorted, or thinly-traded stocks can be "hard to borrow", rates of 5%, 20%, or even higher per annum, applied daily. For a stock with a 50% annualised borrow rate, a short position held for one week costs roughly 1% just in borrowing costs, before considering any price movement. The difficulty of finding borrows can itself become a market signal: rising borrow rates indicate increasing short interest and limited available supply.

Short recall risk. The lender can recall their shares at any time (with short notice). If the lender sells their shares or instructs their custodian to recall the loan, the short seller must return the shares immediately, either by buying in the open market (a buy-in) or finding a new lender. In volatile markets, recalls at inopportune moments can force short sellers to cover at bad prices.

Settlement obligation. At settlement (T+1 in the US), the short seller must deliver the shares. They do not own them, they borrowed them. Their clearing position shows a negative (short) holding. The CCP ensures delivery; if the short seller fails to deliver, the failed settlement process applies.

Why this matters for exchange developers. The exchange's matching engine processes short sales exactly like any other sell order, the distinction between a short sale and a long sale is invisible at the order book level. The matching engine does not know or care whether the seller owns the shares. The borrow and locate process happens entirely outside the exchange, in the prime brokerage and custody infrastructure. However, exchange reporting systems are required to flag short sales (in the US, short sale orders must be marked "short" in the FIX message and this appears in the audit trail), and some regulatory checks at the gateway level confirm the short sale flag is present.

Wall Street¶

Wall Street is named after an actual wall, a wooden palisade built in 1653 by Dutch colonists along the northern edge of their settlement (then called New Amsterdam, now Lower Manhattan) to protect against British and Native American incursions. The wall is long gone; the street that replaced it became the financial centre of America, and now "Wall Street" is a metonym for the entire US financial industry, regardless of where the actual firms are physically located.

Why This Matters for You¶

When you encounter a term in the codebase that seems oddly concrete for a piece of software, "the book," "the tape," "the spread," "the floor price," "tick by tick", the reason it sounds physical is that it was physical. These words have been used continuously, with the same meanings, through every technological revolution the industry has undergone, because the underlying concepts remained constant even as the implementation changed completely.

This is also why you will find financial terminology resistant to renaming even when better alternatives exist. Saying "priority queue" instead of "the book" would be technically precise but professionally unintelligible. Finance is a conservative industry with deep institutional memory, and the vocabulary is part of that memory. Learning the words, and where they came from, is learning the culture.

The Participants¶

Before diving into mechanics, it helps to know who is actually in the room.

Traders and Investors¶

The broadest category of participant is anyone who buys or sells for themselves, whether they are profit-seeking or managing risk.

Retail investors are individuals trading their own money, typically through brokerage apps (Robinhood, Fidelity, Schwab, eToro). Retail orders tend to be small (a few hundred shares at most), arrive randomly throughout the day, and , critically , are considered uninformed flow by market makers, meaning they are statistically unlikely to be based on superior information about the company's near-term prospects. Retail flow is therefore profitable to serve: the spread can be captured with low adverse selection risk.

Institutional investors are organisations managing money on behalf of others: pension funds, mutual funds, hedge funds, insurance companies, sovereign wealth funds, endowments. They trade in sizes that can move markets , a pension fund rebalancing its portfolio may need to buy or sell millions of shares over days or weeks without moving the price against itself. Their orders are typically routed through execution desks that use VWAP algorithms, dark pools, and smart order routing to minimise market impact. The largest institutional investors (BlackRock manages over $10 trillion in assets [1]) have more market influence than many sovereign nations.

The distinction between retail and institutional matters for exchange designers because the two populations have different latency tolerances, different order sizes, different information sets, and different legal frameworks governing their trading. Payment for Order Flow (PFOF) exists because retail flow is genuinely more profitable to service than institutional flow, and this shapes the routing decisions of retail brokers.

In exchange terminology, when a participant submits an aggressive order that immediately executes against a resting order in the book, they are called a taker , they are "taking" liquidity that was already available. The participant whose resting order was filled is the maker (they "made" liquidity available).

High-Frequency Trading (HFT) and Proprietary Trading Firms¶

A distinct and important participant type that does not fit neatly into the retail/institutional or maker/taker classification is the high-frequency trading (HFT) firm and broader class of proprietary trading firms (often called "prop shops").

These firms trade entirely for their own account, with their own capital, using automated strategies. They do not manage client money and do not act as brokers. Well-known firms include Citadel Securities, Virtu Financial, Jane Street, Jump Trading, and IMC. Some (like Citadel Securities and Virtu) are primarily market makers; others run arbitrage and statistical arbitrage strategies.

HFT firms are estimated to account for approximately 50% of equity trading volume on US exchanges [1], and a significant portion of derivatives volume. They make markets extremely tight (narrow spreads) in liquid products because competition between HFT market makers is intense. They also create controversy: critics argue that latency arbitrage gives them an unfair structural advantage over slower participants; defenders argue that their market making activity lowers costs for everyone.

For exchange developers, HFT firms are the most technically demanding participants. Their latency requirements drive the design of co-location services, the nanosecond timestamping standards, and the deterministic processing guarantees that define high-performance matching engine architecture. When an exchange system must process millions of messages per second with microsecond response times, it is largely because HFT participants require it.

Market Makers¶

This is a concept worth understanding deeply, because it is central to how exchanges actually work in practice, and because the exchange system you are building contains a significant amount of code dedicated specifically to managing market makers.

A market maker is a professional participant who continuously quotes both a buy price and a sell price for an instrument. They are simultaneously willing to buy from anyone who wants to sell, and to sell to anyone who wants to buy. In exchange for taking on this obligation, they earn the spread, the small gap between the price they will buy at and the price they will sell at. Market makers are the reason you can usually buy or sell a stock immediately without waiting for a human counterparty to appear. Their standing orders are already in the book, waiting.

NYSE has what it calls Designated Market Makers (DMMs), specific firms assigned to each stock with obligations to maintain fair and orderly markets. Nasdaq calls them Market Makers. Eurex, the European derivatives exchange, runs a formal Market Making Programme with contractual quoting obligations. When a market maker's resting order is later filled by someone else's incoming order, the market maker is called a maker (they "made" liquidity available). The person whose order triggered the fill is the taker. Exchanges frequently give makers a fee rebate and charge takers a fee, to incentivise the provision of liquidity.

Key idea: Market makers earn the spread by continuously providing two-sided quotes, a standing bid and ask, making it possible for others to trade immediately at any time. They are not passive: their position changes with every fill, and they must manage inventory and information risk in real time. The Market Makers section of Part II examines the full operational detail: formal obligations, what happens when a quote is hit, protection mechanisms, and the software implications of supporting them.

Brokers¶

Broker itself is an old word. The word "broker" traces back to Middle English (brocour) and Anglo-Norman (abrocour), originally referring to a middleman, small trader, or wine merchant. It referred originally to a person who "broaches" (opens) a cask and sells the wine retail, an intermediary between producer and consumer. By the late medieval period it had generalised to any trade intermediary, and it has carried that meaning into finance.

A broker does not trade for their own account. They act as an intermediary: they receive orders from clients and submit them to the exchange on the client's behalf. Retail brokerages (Fidelity, Schwab, eToro) aggregate small orders from millions of individuals. Institutional brokers (Goldman Sachs, Morgan Stanley, JPMorgan) execute large block orders for institutional clients with minimum market impact.

Prime brokers are a specific tier of broker providing a package of services to sophisticated clients, primarily hedge funds: securities lending (enabling short selling), leveraged financing, consolidated clearing and custody across multiple brokers, and sometimes execution services. Without a prime broker relationship, a hedge fund could not efficiently short sell or use leverage. The major prime brokers are divisions of the large investment banks.

The Exchange Itself¶

The exchange is not a passive infrastructure provider. It is a regulated entity that enforces rules, monitors for manipulation, reports trades to regulators, and ensures the market functions fairly. In many jurisdictions, exchanges are themselves public companies listed on exchanges (NYSE's parent company, ICE, is listed on NYSE; NASDAQ lists on Nasdaq).

A significant historical shift: exchanges used to be member-owned mutuals, non-profit organisations run for the benefit of their broker-dealer members. Over the past 30 years, most major exchanges have demutualised, converting to for-profit public companies. NYSE demutualised and listed in 2006; London Stock Exchange demutualised in 2001. This shift changed the incentive structure of exchanges: they now compete for order flow and listing fees, and their technology investment decisions are driven partly by shareholder returns.

Regulators¶

Regulators are not participants in the traditional sense, they do not submit orders, but they are the most consequential stakeholders in exchange system design. Every audit trail format, kill switch requirement, pre-trade check, and trade report exists to satisfy a regulatory obligation.

In the US, the SEC oversees equity exchanges and broker-dealers. The CFTC oversees futures and derivatives exchanges. FINRA (Financial Industry Regulatory Authority) is a self-regulatory organisation that oversees broker-dealers. Exchanges themselves are also self-regulatory organisations (SROs): they have obligations to monitor their own markets and report suspicious activity.

Internationally: the FCA (Financial Conduct Authority) in the UK, ESMA (European Securities and Markets Authority) and national regulators under MiFID II in the EU, the FSA in Japan, the SFC in Hong Kong, and ASIC in Australia.

For exchange developers, the practical implication is that regulatory requirements are non-negotiable features. A matching engine that produces a legally insufficient audit trail is not a working matching engine, regardless of its throughput. Understanding which regulator and which ruleset governs a given exchange is part of the technical specification.

Note, quotes vs orders: Throughout this document, the terms "order" and "quote" are sometimes used to describe resting instructions in the book. Operationally they are different: a quote is a two-sided bid/ask pair submitted by a market maker (a single instruction generating two linked legs), while an order is a one-sided instruction submitted by any participant. A quote may internally generate one or two order records with linked identifiers; quote IDs and order IDs may differ. The Market Makers section of Part II covers this distinction in detail.

A Brief Tour of Real-World Exchanges¶

To ground these concepts in reality, here is a brief overview of the exchanges most relevant to exchange system developers.

NYSE (New York Stock Exchange)¶

Founded in 1792, NYSE is the world's largest equity exchange by market capitalisation of listed companies. Its founding is traced to the Buttonwood Agreement of 17 May 1792, when 24 stockbrokers signed a document under a buttonwood tree on Wall Street agreeing to trade securities only among themselves and at fixed commission rates [10]. This agreement established the principle of a closed, rule-governed professional market , the model that all regulated exchanges follow today.

NYSE is a hybrid market: it combines electronic order matching with Designated Market Makers (DMMs) who have responsibilities to maintain fair and orderly markets and can intervene manually in certain situations. NYSE uses price-time priority and runs opening and closing auctions. Its closing auction is among the most important pricing events in global finance, determining the official closing prices that benchmark trillions of dollars of fund performance.

Despite being the iconic "stock exchange," NYSE handles only a fraction of total US equity volume. Due to fragmentation under Reg NMS, NYSE typically accounts for roughly 20–25% of US equity volume [1]; the rest routes to NASDAQ, Cboe, and dozens of other venues. This is not a sign of weakness , it reflects the fragmented, competitive nature of modern US equity markets.

NASDAQ¶

NASDAQ launched in 1971 as the world's first fully electronic stock exchange. It is home to many of the world's largest technology companies (Apple, Microsoft, Amazon, Google). NASDAQ is a pure electronic market, no floor traders, no DMMs in the traditional sense. It pioneered the technology approach to exchange operation and drove down transaction costs dramatically.

CME Group (Chicago Mercantile Exchange)¶

CME Group is the world's largest futures exchange, operating CME, CBOT (Chicago Board of Trade), NYMEX, and COMEX. Futures contracts on everything from interest rates to agricultural commodities to weather indices trade here. CME uses the Globex electronic trading platform, which processes millions of orders per day. CME uses both price-time priority and pro-rata allocation depending on the product.

Eurex¶

Part of Deutsche Börse Group, Eurex is Europe's largest derivatives exchange, headquartered in Frankfurt. Eurex is known for its sophisticated market making programmes and its strict but fair treatment of high-frequency trading. The Eurex T7 trading system is used by multiple exchanges globally. Eurex introduced the concept of formally structured market maker obligations with MMP protection.

LSE (London Stock Exchange)¶

The LSE is one of Europe's oldest exchanges, dating to the 17th century coffee houses. It trades equities, bonds, and ETFs. The LSE uses the SETS (Stock Exchange Electronic Trading System) for liquid equities and runs opening and closing auctions. The LSE's Millennium Exchange technology platform is used by dozens of exchanges globally.

Historic Note: The Big Bang, 27 October 1986

The modern LSE is largely the product of a single day of deregulation known as the Big Bang. Until 1986, the LSE operated under a cartel-like structure inherited almost unchanged from its coffee-house origins: brokerage commissions were fixed by rule rather than set by competition, and firms were legally separated into brokers (who dealt with clients) and jobbers (who traded as principals on the floor), with outside and foreign ownership of member firms tightly restricted. On 27 October 1986, all of this changed at once: fixed commissions were abolished, the broker/jobber distinction was scrapped, non-member and foreign ownership was permitted, and open-outcry floor trading was replaced almost overnight by the screen-based SEAQ electronic quotation system. The changes were bundled together deliberately, as a negotiated settlement of a long-running restrictive-practices case brought by the UK government against the exchange, and the government wanted them delivered as a single event rather than a gradual transition. The effect was to compress a decade of gradual American-style deregulation into one day, and it is the direct reason the LSE moved from a floor-based, fixed-commission market to the electronic, competitive one described in this document.

Big Bang has an almost exact American predecessor: on 1 May 1975 ("May Day"), the SEC abolished fixed brokerage commissions on the NYSE, ending nearly two centuries of fixed-rate trading that dated back to the original 1792 Buttonwood Agreement described earlier in this chapter. Commission rates had been fixed by NYSE rule for so long that the change was existential for many old-line brokerages; it also created the discount-brokerage industry (Charles Schwab was founded the same year) and set in motion the competitive, cost-conscious order-routing dynamics, including, decades later, payment for order flow, that the Smart Order Routing section of Part IV describes in detail. May Day and Big Bang are worth holding in mind together: eleven years apart, one American and one British, both replacing a fixed-price professional cartel with open price competition, and both direct ancestors of the fee-driven, technology-mediated market structure this book describes throughout. [U.S. Securities and Exchange Commission historical release on the elimination of fixed commissions, 1975; London Stock Exchange Group, Big Bang 1986 historical retrospective.]

Euronext¶

Euronext is Europe's largest exchange group by number of listed companies, operating markets in Amsterdam, Brussels, Paris, Lisbon, Dublin, Oslo, and Milan. Originally formed in 2000 by the merger of the Paris, Amsterdam, and Brussels exchanges, it expanded significantly through subsequent acquisitions including the Milan Stock Exchange (Borsa Italiana) in 2021. Euronext uses the Optiq trading platform and operates under MiFID II. Its Amsterdam exchange is historically notable as the successor to the world's first stock exchange (the Amsterdam Exchange, 1602).

Nasdaq Stockholm (Stockholmsbörsen, STO)¶

Nasdaq Stockholm is Sweden's primary regulated securities exchange and one of the core venues in the Nordic region. The original Stockholm Stock Exchange dates to 1863, and the modern market became part of the Nasdaq group through Nasdaq's acquisition of OMX in 2008. Today, Nasdaq Stockholm operates as part of the wider Nasdaq Nordic market structure alongside Copenhagen, Helsinki, and Icelandic venues.

For exchange developers, Nasdaq Stockholm is a useful real-world reference because it combines deep local equity liquidity with a highly standardised pan-Nordic technology model. The market is fully electronic, supports auction phases (including opening and closing auctions), and runs under the same MiFID II transparency and best-execution regime as other EU venues.

The venue's best-known benchmark is the OMXS30 index, which tracks the 30 most traded shares on Nasdaq Stockholm. The exchange is the home listing venue for many major Swedish and Nordic companies, including names such as Ericsson, Volvo, Atlas Copco, and Investor AB, making it central to Nordic equity price discovery.

From an infrastructure perspective, Nasdaq Stockholm aligns with broader Nasdaq market technology standards (including INET-based matching architecture for cash equities) and interoperates with regional post-trade infrastructure such as Euroclear Sweden for securities settlement. In practical terms, this makes it a strong example of how a national exchange can preserve local market identity while operating inside a larger cross-border technology and regulatory framework.

IEX (Investors Exchange)¶

IEX launched as a dark pool in 2013 and became a registered national securities exchange in 2016. It is the exchange that popularised the speed bump: a deliberate 350-microsecond delay applied to incoming orders, designed to level the playing field between HFT latency arbitrage strategies and slower institutional investors. IEX was the subject of Michael Lewis's 2014 book Flash Boys, which brought widespread public attention to HFT and exchange structure debates.

The speed bump attracted significant institutional support from large asset managers who believed it reduced predatory latency arbitrage. However, IEX has consistently captured a relatively small share of US equity volume (typically 2–3%) [1], suggesting that the speed bump's appeal did not translate into dominant market share. Whether this reflects genuine limitations of the model or simply the difficulty of displacing entrenched incumbent exchanges remains debated in market structure circles. IEX remains disproportionately influential in regulatory discussions given its size, having prompted rule-making discussions at the SEC around speed bumps and exchange access fees.

Cboe (Chicago Board Options Exchange)¶

Cboe is the world's largest options exchange, operating Cboe, C2, BZX, BYX, EDGX, and EDGA exchanges. Cboe invented the listed options market in 1973. It calculates the VIX (Volatility Index, the "fear gauge" of the market) from options prices.

JPX (Japan Exchange Group)¶

JPX was formed in 2013 by merging the Tokyo Stock Exchange (TSE) and Osaka Securities Exchange. It is consistently one of the world's largest exchanges by market capitalisation of listed companies, generally ranked just behind NYSE and NASDAQ and close to Shanghai, though the precise ordering shifts from year to year and depends on whether Shanghai and Shenzhen are counted as one market or two, so any "top three" claim should be checked against a dated source (e.g., World Federation of Exchanges statistics) rather than treated as fixed. JPX operates on an all-electronic platform called arrowhead. Japanese markets have their own session structure, tick size rules, and circuit breaker conventions; the daily price limit system (where trading in a stock is suspended if it moves more than a set amount from the previous close) differs from the US LULD approach.

HKEX (Hong Kong Exchanges and Clearing)¶

HKEX is the primary exchange for Hong Kong-listed equities and also provides the main electronic gateway for mainland China stocks through the Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect programmes. Stock Connect allows international investors to trade China A-shares (mainland China stocks) and allows mainland investors to trade Hong Kong-listed stocks through a northbound/southbound quota system, a unique regulatory and technical arrangement that requires matching engines on both sides to coordinate.

SGX (Singapore Exchange)¶

SGX is Southeast Asia's largest exchange, trading equities, derivatives, and fixed income. It is notable as a hub for Asian futures contracts, Nikkei 225 futures, MSCI Asia index futures, and iron ore contracts all trade on SGX. SGX acquired Scientific Beta (factor indices) and has invested heavily in data analytics services alongside its exchange operations.

ASX (Australian Securities Exchange)¶

ASX serves the Australian equity and derivatives markets. It became notable in the technology community for its attempt to replace its CHESS (Clearing House Electronic Subregister System) settlement platform with a blockchain-based system, a project that was eventually cancelled in 2022 after years of development, at significant cost. The cancellation is a cautionary tale for exchange technologists about the risks of replacing proven settlement infrastructure with unproven technology.

Listing and Delisting Mechanics¶

The Before the Exchange section described the IPO from the company's side: underwriters, roadshows, pricing. This section closes the loop from the exchange's side. Going public is not just a financial event, it is an application to a specific exchange, governed by that exchange's own rulebook, and staying listed is an ongoing obligation, not a one-time achievement.

Why Exchanges Compete for Listings¶

A listing is valuable to an exchange for reasons beyond the one-off listing fee. A listed company generates ongoing order flow (every share ever traded on that exchange contributes to trading revenue), market data revenue (see Market Data Economics in Part IV), and prestige that attracts further listings. This is why exchanges actively court companies before an IPO, and why the choice between, say, NYSE and NASDAQ for a marquee technology company is itself a competitive sales process, not a formality.

Initial Listing Standards¶

Every exchange publishes initial listing standards, minimum quantitative and qualitative thresholds a company must meet before its shares can begin trading. These typically combine several dimensions, and both NYSE and NASDAQ offer multiple listing tiers with different thresholds (NASDAQ's Global Select, Global Market, and Capital Market tiers, for example, from most to least stringent):

- Minimum share price: commonly a bid price of at least $4.00 at initial listing.

- Market value of publicly held shares (public float): a minimum aggregate dollar value of shares actually available for public trading, excluding insider- and affiliate-held blocks, illustratively in the tens of millions of dollars for the least stringent tiers and considerably higher for the most prestigious ones.

- Minimum number of round-lot shareholders: a floor on how widely the shares are already held, intended to ensure a genuine public market exists from day one rather than a handful of large holders.

- Corporate governance requirements: an independent board majority, an independent audit committee, and public financial disclosure obligations under the exchange's rules and the applicable securities laws.

(Exact numeric thresholds are revised periodically by each exchange and its regulator; treat the figures above as illustrative of the kind of requirement, not as current values to hardcode into any reference-data system.)

Meeting every quantitative threshold is necessary but, on some exchanges, not sufficient: as the Indexes section of Part II noted for S&P 500 committee discretion, initial listing approval can involve qualitative judgement about the business and its readiness for public markets, not a purely mechanical checklist.

Continued Listing: An Ongoing Obligation¶

Initial listing standards get most of the public attention, but continued listing standards matter more to exchange system developers, because they generate ongoing, automated compliance monitoring rather than a one-time gate. A company that met every threshold at its IPO can fall out of compliance years later if its stock price declines, its market cap shrinks, or its public float narrows.

The most common continued-listing trigger is the minimum bid price rule: if a stock's closing price stays below $1.00 for 30 consecutive trading days, the exchange issues a formal deficiency notice. The company then has a cure period, commonly 180 days, to regain compliance (ten consecutive trading days at $1.00 or above), and in some cases a further 180-day extension if it meets other listing criteria. This is the direct, practical reason struggling companies execute a reverse stock split (see the Corporate Actions section of Part IV): consolidating, say, ten existing shares into one instantly multiplies the nominal share price by ten, curing a bid-price deficiency without changing the company's actual market value by a cent. A reverse split undertaken for this reason is a compliance action, not a statement about the business, and exchange systems must handle it exactly like any other corporate action (adjusting resting orders, historical price series, and reference data) regardless of the reason behind it.

Failure to cure within the allowed window leads to involuntary delisting: the exchange begins the formal process of removing the security, the company can appeal to a listing qualifications panel, and if the delisting proceeds, the shares typically continue trading, if at all, on the OTC (over-the-counter) markets described in Part I, with materially less liquidity, visibility, and investor protection than an exchange listing provided.

Voluntary Delisting¶

Not all delistings are compliance failures. A company can voluntarily delist because it has been acquired (its shares convert to cash or acquirer stock, as described in the Corporate Actions section of Part IV), because it has been taken private (a controlling investor or management buyout removes public shares from circulation entirely), or, more rarely, because it decides the costs of public-company reporting and exchange fees no longer justify the benefits of a listing. All of these still require an orderly unwind of open orders and positions in the symbol, exactly as described in the Corporate Actions section, whether the delisting is voluntary or forced.

Alternatives to the Traditional IPO¶

The underwritten IPO described in Part I, banks buy the offering and guarantee the company its proceeds, is not the only path onto an exchange.

Direct listings. In a direct listing, a company's existing shares begin trading directly on the exchange with no new shares issued, no underwriter guarantee, and no fixed offer price set in advance by a roadshow. Instead, the opening trade is established through the exchange's opening auction mechanism (see the Opening and Closing Auction section of Part II) exactly like any other trading day's open, just with unusually intense interest and no underwriter smoothing the process. Spotify's April 2018 listing on NYSE and Slack's June 2019 listing on NYSE were the pioneering examples that established direct listings as a credible alternative for companies that do not need to raise new capital and want to avoid underwriting fees and the traditional IPO discount. Because there is no underwriter-set price to anchor expectations, the exchange's auction-price-discovery mechanism carries unusually high scrutiny on a direct listing's first trade.

SPAC mergers. A Special Purpose Acquisition Company (SPAC) is a shell company with no operating business that itself completes a conventional IPO, raising cash that is held in trust, with the explicit purpose of later merging with a private operating company to take it public. When the merger (a "de-SPAC" transaction) completes, the private company's shareholders receive shares in the (now renamed) public shell, and the target company is effectively listed without ever running its own IPO process. SPACs existed for decades as a niche structure but became a major share of total US listing activity in 2020–2021, before a wave of poor post-merger performance and increased SEC disclosure requirements sharply reduced the volume of new SPAC formations from 2022 onward. For exchange and reference-data systems, a de-SPAC transaction looks much like the symbol changes and delistings described in Corporate Actions, the shell's original ticker and CIK are typically replaced by the operating company's, but compressed into a single scheduled event that must be coordinated precisely across trading, clearing, and market data simultaneously.

Key idea: An IPO is a financial event; a listing is a continuing regulatory relationship with a specific exchange, governed by initial standards to get in and continued standards to stay in. Reverse splits, delistings, direct listings, and SPAC mergers are all variations on the same underlying reference-data and corporate-action machinery described in Part IV, the trigger differs, but the exchange-side mechanics of updating symbols, adjusting orders, and coordinating the change across every downstream system are the same.

Part II: Orders, Matching, and the Trading Day¶

How orders work, how the matching engine processes them, and how a complete trading day unfolds from open to close.

Historic Notes