The Order Book¶

Learning objectives

After reading this page you will understand:

- What an order book is and how it is structured

- The difference between a bid and an ask

- What the spread is and why it matters

- How price-time priority determines who gets filled first

- What happens step-by-step when two orders match

What is an order book?¶

When you buy a share of stock, someone else must sell it to you. But they may not be available at exactly the moment you want to trade, and you may not agree on price. The order book is the mechanism that bridges this gap.

An order book is the live, sorted list of currently executable resting buy and sell orders for one instrument. Conditional orders such as stops are tracked separately until they trigger into executable orders. Every tradable instrument has its own book. Orders are separated into two sides:

| Side | Also called | What it represents |

|---|---|---|

| Bids | Buy side | Traders who want to buy, sorted highest price first |

| Asks | Offer / sell side | Traders who want to sell, sorted lowest price first |

The matching engine continuously checks whether the best bid and the best ask overlap in price. When they do, a trade is produced.

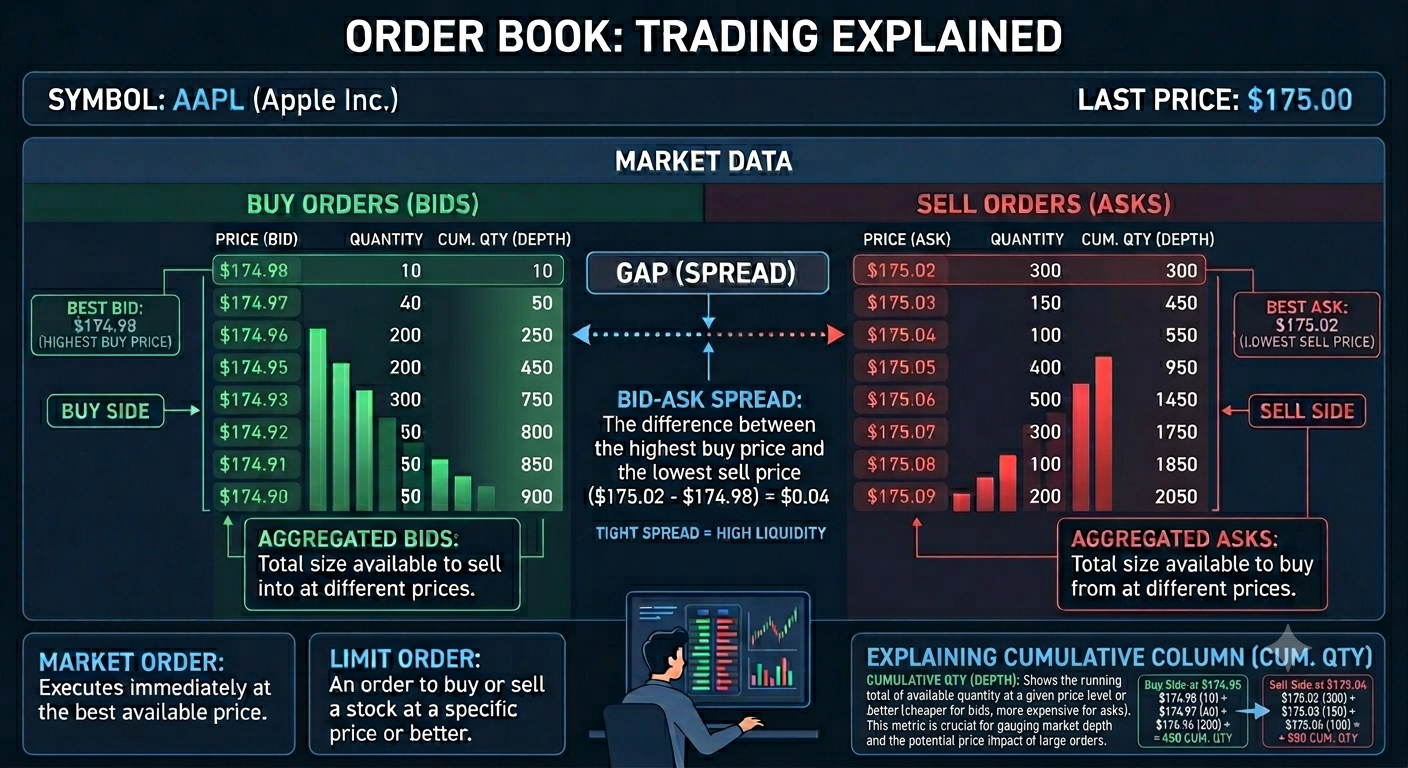

Figure 1: The orderbook.

Figure 1: The orderbook.

A concrete order book¶

Imagine AAPL is trading around $150. The live book might look like this:

BID (buy orders) ASK (sell orders)

───────────────── ──────────────────

Qty Price Price Qty

─── ───── ───── ───

200 149.90 150.10 100

500 149.80 150.20 300

150 149.70 150.30 500

300 149.60 150.50 200

- The best bid (highest buy price) is 149.90 for 200 shares.

- The best ask (lowest sell price) is 150.10 for 100 shares.

- These prices do not overlap — no trade happens yet.

The bid-ask spread¶

The spread is the gap between the best bid and best ask:

The spread represents the cost of an immediate round-trip (buy then sell). A trader who buys at the ask (\(150.10) and immediately sells at the bid (\)149.90) loses $0.20 per share.

Narrow spread (e.g. $0.01) — a liquid market. Many participants are competing to trade, so prices are tight. Cheap to trade in and out.

Wide spread (e.g. $2.00) — an illiquid market. Few participants, or high uncertainty. Expensive to trade in and out.

The mid-price is the midpoint between bid and ask:

Book depth¶

Depth refers to how much volume (quantity of shares) is available at or near the top of each side. A deep book absorbs large orders without moving the price much. A thin book has little resting quantity and even a moderate order can push the price significantly.

Looking at our example book above, if a trader submits a market sell order for 600 shares, it would: 1. Fill 200 shares at the best bid of 149.90 2. Fill 400 shares at the next level, 149.80

The average fill price would be:

The trader wanted to sell at ~149.90 but the large size caused the actual average to be 149.83. This difference is called slippage.

Price-time priority¶

When multiple orders rest at the same price, the matching engine must decide which one fills first. EduMatcher uses price-time priority (also called FIFO priority):

- Price first — the order with the best price for the counterparty fills first. For bids: the highest price wins. For asks: the lowest price wins.

- Time second — among orders at the same price, the one that arrived earliest fills first.

Worked example — three bids at the same price¶

Suppose three traders each submitted a LIMIT BUY at exactly $149.90:

| Order | Trader | Time submitted | Qty |

|---|---|---|---|

| A | GW01 | 09:30:01.100 | 100 |

| B | GW02 | 09:30:01.250 | 200 |

| C | GW03 | 09:30:03.900 | 150 |

Now a LIMIT SELL at $149.90 for 250 shares arrives. The engine processes bids in time order (A before B before C):

- Order A (GW01, 100 shares) fills first — submitted earliest.

- Order B (GW02, 200 shares) — only 150 more needed, so 150 of the 200 fills, leaving 50 shares of Order B resting.

- Order C (GW03) — gets nothing this time; it was last in queue.

The result:

| Order | Fill | Remaining |

|---|---|---|

| A | 100 | 0 (fully filled) |

| B | 150 | 50 (partially filled, still resting) |

| C | 0 | 150 (still resting, behind Order B in queue at this price) |

This is why being early matters: all else being equal, the first order in queue has an advantage. This creates an incentive for market participants to submit orders quickly — one driver of the speed race in modern markets.

Step-by-step: what happens when orders match¶

Here is the full lifecycle of a trade between a resting limit order and an incoming aggressive order.

State: AAPL book has a resting BID from GW01

Action: GW02 submits a SELL LIMIT at 150.00 for 100 shares

Engine processing:

- Incoming order hits the matching engine via ZeroMQ PUSH socket.

- Engine checks: is there a resting bid at or above $150.00? Yes — GW01 at $150.00.

- Trade price is the resting order's price ($150.00) because it was first.

- Engine generates a

trade.executedevent: - buyer: GW01, qty: 100, price: 150.00

- seller: GW02, qty: 100, price: 150.00

- Both orders are fully filled and removed from visible bid/ask levels.

- Engine publishes

order.fill.GW01andorder.fill.GW02to both gateways. - Engine publishes a

book.AAPLsnapshot — that bid level is now gone. - Clearing process receives

trade.executedand updates both traders' P&L.

Result:

GW01: bought 100 AAPL @ 150.00 — position +100, avg cost 150.00

GW02: sold 100 AAPL @ 150.00 — position -100 (or flat if they were long)

Passive vs. aggressive orders¶

An order that rests on the book, waiting for a counterparty, is called passive (or a maker order, because it "makes" liquidity for others to trade against).

An order that crosses the spread and immediately matches against resting orders is called aggressive (or a taker order, because it "takes" available liquidity).

| Role | Also called | What it does |

|---|---|---|

| Passive | Maker / resting | Posts to the book, waits |

| Aggressive | Taker / crossing | Matches immediately against the book |

In real exchanges, makers often pay lower fees than takers as a reward for providing liquidity. EduMatcher does not model fees, but the distinction is important for understanding order strategy.

Key terms summary¶

| Term | Definition |

|---|---|

| Order book | The live, sorted collection of all resting buy and sell orders for one instrument |

| Bid | A resting buy order; bids are sorted highest price first |

| Ask / offer | A resting sell order; asks are sorted lowest price first |

| Spread | Gap between best bid and best ask |

| Mid-price | Average of best bid and best ask |

| Depth | Total resting volume near the top of the book |

| Slippage | Difference between expected and actual average fill price on a large order |

| Price-time priority | Fill ordering rule: best price first, then earliest arrival |

| Passive / maker | An order resting on the book |

| Aggressive / taker | An order that crosses the spread and matches immediately |

Implementation Note: Tick Prices¶

EduMatcher stores prices internally as integer ticks (not floating-point decimals). That means priority, comparisons, and level aggregation are exact in engine code. Displayed bid/ask values are converted back to decimals for user-facing views.